Your cart is currently empty!

Borrowing Without Intent To Repay: How Modern Fiat Currency Systems Concentrate Wealth By Design

The monetary system which we are all subjected to this day in age is diametrically opposed to having a regenerative economy.

Simply put, a regenerative economy cannot exist (or will fail) if the money used to transact within it violates the ethics of 1) Care For The Earth, 2) Care For The People, and 3) Reinvest Surplus Towards Earth Care And People Care. Our modern currency does none of these things – in fact the system is structured to actively work against them by design.

This article contains an illustrated, step-by-step visual guide that walks us through how currency is actually created today. By it’s end, our hope is that you’ll agree that if we are to ever create a substantive move towards a truly regenerative ‘de-growth’ economy, we simply must change our monetary system.

In short, the currency (not the same as money, as we’ll explore) we are forced to use today is created via fraud – one committed at such a scale and obfuscated by the intentionally complicated language of officialdom that the vast majority of people have no idea how it actually works (i.e. how they are being stolen from and their children indebted without their consent) – every minute of every hour of every day.

Most people have heard that our currency is “printed out of thin air” and are vaguely aware of inflation as a threat to their savings. In this post, we aim to illustrate exactly how this fraud works. We believe once an individual truly understands the fraud being perpetrated against them, they can begin to take concrete actions to spread that awareness, protect themselves and their families, and redirect their own life energy away from those institutions that are a one-way drain on society and into closed-loop regenerative systems that create true wealth and opportunity for themselves, their surrounding community, and the global human community at large.

First, we need to begin by defining the difference between money and currency. They are not the same, as demonstrated below.

Money vs. Currency – How They Differ

Our true wealth is our time and freedom. Time and freedom are what we trade for money. Money is a container to store individual and collective economic energy until it is ready to be deployed – a “claim check” on life energy. Currency robs us of time and freedom because it lacks one of the necessary qualities of money.

There are six qualities that any form of functional currency must have, and one additional quality that differentiates currency from money:

Currency must be…

- A medium of exchange – many people have access to it in order to trade it.

- A unit of account – each unit “holds” a known amount of value.

- Portable – easy to use and transport (essential for commerce).

- Durable – can’t be easily destroyed.

- Divisible – can make change.

- Fungible – interchangeable, a dollar in my pocket buys the same as a dollar in your pocket.

Money is everything that currency is PLUS…

- A store of value – money stores the life energy that went into obtaining it over long periods of time.

Because currencies can be printed at will by governments, the existing currency supply is continually being diluted with freshly created currency, making the dollars in your bank account or wallet worth less with each passing second. In fact, the dollar has lost over 96% of it’s purchasing power since 1913, the year in which the Federal Reserve (the U.S.’s central bank) was created and a national income tax was legislated (quite nefariously too, but that’s for another post). For an excellent primer on the difference between money and currency, we recommend watching Episode 1 of The Hidden Secrets Of Money by Mike Maloney below.

Now that we know the difference between currency and money, let’s go step-by-step through the fraud that is our modern monetary creation mechanism and learn how it is perpetrated by governments and the banking sector to enrich the few while robbing from the many.

How Modern Debt-Backed Fiat Currency Is Created (i.e. Steals Life Energy And Creates Wealth Inequality)

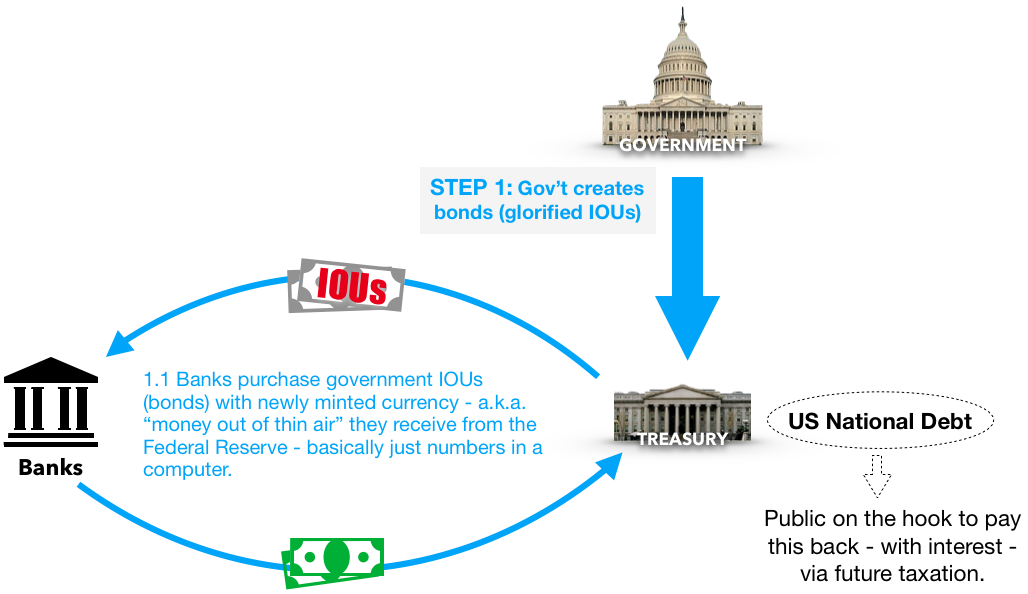

Step 1: The Government Creates Glorified IOUs

Politicians like to spend more than their income (taxes). People like it too (at least in the present moment) because they get to spend future prosperity today – no big deal, we’ll worry about the bill tomorrow! This is called deficit spending.

In order to fund this deficit, the Treasury issues a bond, essentially a promise (glorified IOU) that if you give us $100 today we’ll repay you that $100 plus interest at some set time in the future. These bonds / promises / glorified IOUs are called treasuries and are paid back via taxation.

Treasuries are sold at auction to the big banks (“primary dealers”), who either earn interest by holding the bond, or more typically re-sell these bonds to the Federal Reserve (the central bank of the United States).

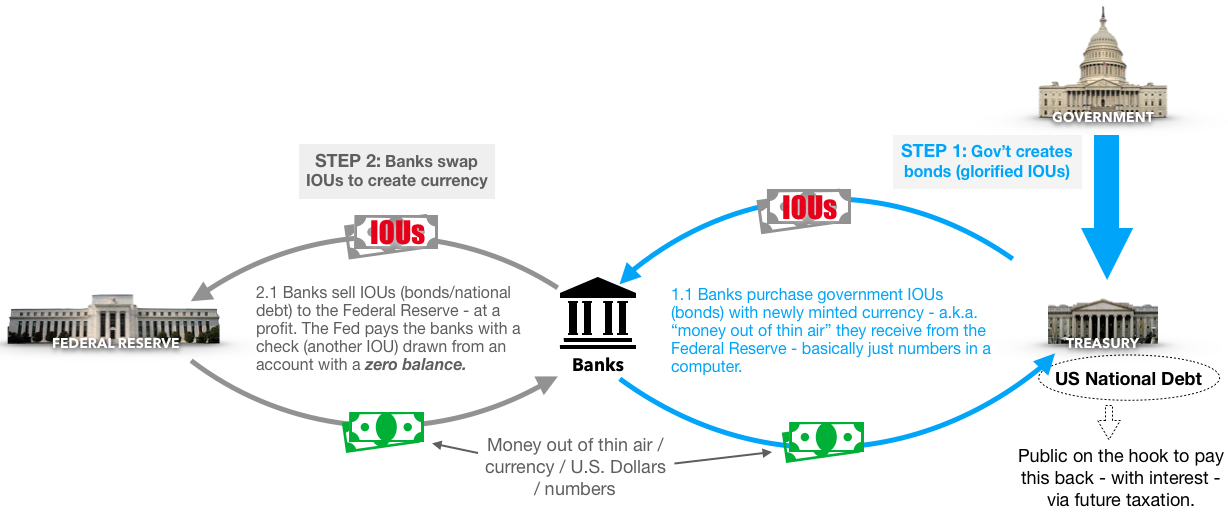

Step 2: The Banks Create Currency By Swapping IOUs

The Federal Reserve (from hereon referred to as the Fed) purchases these bonds from the big banks at a guaranteed profit by writing the banks a check (another glorified IOU) drawn on an account with a zero balance.

You read that right. The Fed has a bank account with a big fat “0” in it, and they use that account to write a check (made up numbers) to buy government issued debt (bonds/glorified IOUs/promises) from the primary dealers (big banks) who initially purchased them at auction from the Treasury.

If you prefer a narrated video walkthrough, check out Chapter 8 of Peak Prosperity’s Crash Course below.

Step 3. Government Spends The Numbers

The Treasury distributes these numbers (now called dollars) that it receives from the banks via the Fed in exchange for its promises (government bonds) to the alphabet soup of government agencies where it is spent by politicians (some elected, mostly non-elected).

The government spends in three main categories – public works, social programs and war.

The government employees, contractors and soldiers who build the public works, run the social programs and go to war are paid in these numbers (now called dollars) which they deposit in a bank.

Once these numbers (dollars) are deposited in the bank they are not held in trust for the account holder. Instead, they are loaned out by the bank in a process called…

Step 4. Fractional Reserve Lending

Banks are only required to hold a 10% reserve against their total deposits. This means that if you deposit $100 into your account, the bank only has to keep 10% of that on hand (called vault cash, just in case you want some) – the other 90% it is free to loan out. This is called Fractional Reserve Banking. The bank replaces the $90 it takes from your account with bank credit – another made up IOU.

The bank then loans out $90 of your initial $100 deposit. There are now $190 in “existence” from an initial deposit of $100. The borrower will take the money lent to him, go and make a purchase (house, car, business investment etc.) and pay the seller with the $90 from your initial $100 deposit. The seller then deposits his $90 into a bank account, and that bank now loans out $81 (90%) of that deposit. There are now $271 in circulation.

And so on it goes, until ultimately a $100 cash deposit creates $1,000 in new, circulating currency.

NOTE: The banking sector's use of fractional reserve lending the primary engine of currency creation in modern fiat currency systems. It is estimated that 92-96% of all currency in circulation today is created by the banks, not the government (Steps 1-3). When a commercial bank loans an individual money, they create new deposit dollars in accounts on their books in exchange for a borrowers IOU. Said more simply, when you go get a loan from a bank to make a purchase, they literally type numbers into your account (and you have to pay back those made up numbers with interest).

This is the mechanism by which the value of the currency is constantly being diluted with newly created “thin air” currency. The prices of everyday goods and services act as the sponge to soak up this inflating currency supply – as evidenced by the constantly rising nominal costs of living, food, health care, transportation, home ownership and more.

Is this fish starting to smell yet? Just wait, it gets even better.

Step 5. Our Numbers Are Taxed

Nearly all humans on the planet in one form or another trade their time and freedom for currency – most of us call this “going to work”.

By now you might feel itchy and bothered – we literally trade our true wealth (time and freedom) for numbers that have quite literally been typed into a computer. The only reason we continue to do so is that those numbers represent our blood, sweat, tears, labor, ideas and talent. WE, as individual members of the U.S. tax-paying collective, are what gives our currency value.

It doesn’t stop there, however. Every Ponzi scheme needs some flow of capital in order to repay earlier suckers. Our currency system works the same way.

We work hard, save and scrimp, then pay huge sums to the tax collector (Internal Revenue Service – IRS). The IRS then gives all of the numbers it collects (forcibly requests? steals?) to the Treasury. The Treasury pays back principal and interest on all of the bonds (promises/IOUs) held by the Fed that the Fed bought from the Treasury with a fraudulent check drawn on an account with nothing in it!

Ever increasing amounts of the total taxes collected each year in the United States go towards servicing the debt (i.e. paying back principal and interest on previously issued debt). This is why the federal income tax was instituted in the same year as the Fed was created – they need each other!

A NOTE ON DEBT CEILING THEATER: In order for this system not to collapse it must always grow. And because every new dollar created is backed only by debt on which interest is due, there can never be enough dollars in existence to pay down the debt. The currency supply must continue to grow exponentially in order to service the constantly compounding debt load, until one day when it will all collapse under its own weight.

There is a bit of political theater revisited every so often (with increasing frequency as we near the end game for this system) called the Debt Ceiling. Supposedly, the Debt Ceiling limits the amount of debt our government can issue. This is preposterous, as for the system to function debt must always increase. For this reason the debt ceiling is always hemmed and hawed about, but always increased, because there is no other option - either increase the debt or collapse the economy.

When debt is paid down currency is destroyed. When debt and currency meet they annihilate one another. If we paid only the principal (never mind the interest) on all outstanding debt the entire currency supply would vanish. This means that paying down our debt and living within our means is impossible without collapsing the economy. We quite literally have to pay tax just to have a monetary system in the form we do!

Now, let’s discuss how the taxes that we pay (the life energy that is taken from us under threat of violence) are being siphoned towards those who own the system…

Step 6. The Fed’s Secret Owners Take Their Cut(s)

The Federal Reserve is not a government agency. Federal agencies cannot have stockholders. The Fed has stockholders. A piece of stock is a piece of ownership in a company, thus stockholders are owners of a corporation.

The United States Federal Reserve is a private bank.

The Fed pays out an annual 6% dividend to its stockholders.

Who owns the Fed? Who are the stockholders??

This information is tightly guarded, and has been obscured over the 100+ years since the Fed was created. Upon its creation, the Federal Reserve issued stock to the largest banks in the United States. Mergers and acquisitions over the decades have made tracing who actually owns the stock impossible, and the Fed does not make this information public.

Very likely, the owners of the Fed are the primary dealers – the big banks that are first in line at the currency-creation buffet – the same big banks that sell bonds to the Fed (the corporation they own) at a guaranteed profit in exchange for checks drawn against an account with a zero balance (made up numbers), numbers that we then work for to pay taxes to pay the interest on those bonds held by the Fed which is payed out as a 6% dividend to the Fed’s owners (the big banks).

Sounds like financial incest to me, but that is how it works (for now).

“By this means government may secretly and unobserved confiscate the wealth of the people and not one man in a million will detect the theft.”

– John Maynard Keynes

Here it is, all in one picture. You can download a high-definition version as a PDF below

Death By Inflation – The Fate Of All Fiat Currencies

There is no example in all of human history of a fiat currency that has survived and retained its value.

They have all failed.

Gone to zero, every last one.

Finally reduced to what they are – paper backed by no intrinsic value.

Should we assume that our current debt-backed fiat currency system will be any different?

The math bears out the inescapable truth. The system will work until it doesn’t any more. And then the Federal Reserve and the U.S. government will do what those in positions of power have always done, throughout human history when faced with a pay-now-or-pay-later choice.

They’ll kick the can. Again and again for as far and as long as they can.

The powers that be will kick the can by inflating the currency (even more than they are right now). Inflation is experienced by most people as rising prices – but what actually causes inflation is too much money chasing around too few goods – and hence, prices go up. Peak Prosperity has an excellent primer on what inflation really is and how it works below.

Inflation allows the government to pay back the debts of yesterday with today’s dollars that are worth less than yesterday – i.e. the debts are nominally repaid, but with dollars that don’t buy as much as they used to. Government will do this until a critical mass of people can’t pretend to trust the system any longer (usually because they can’t afford food) and the entire system collapses under a mountain of unserviceable debt.

This begs the question “How much time do we have left?”

How much time do we have until it is readily apparent to a critical mass of people that our currency has no value and it ceases to function as a medium of exchange?

While impossible to say with exact certainty, we know enough to say that we are close – certainly within the decade (if historical currency implosions have anything to say about it), very likely within several years, and very possibly any day now.

It is highly instructive to look at a brief history of currency in the U.S. to get an idea of how past financial crises have come about and been resolved. While the timing is impossible to predict, the signs of impending systemic dysfunction rhyme from bust to bust.

One potential way in which things might play out – known as the “ka-POOM” theory – indicates that based on past hyperinflationary events, we will first experience a deflationary period / event that will trigger the currency-printing response by the Fed that will ultimately lead to hyperinflation.

Very recently in mid-April of 2020, the United States (and many other countries as well) sent most of its citizens a $1,200 check as part of the first of what will undoubtedly be many coronavirus related economic stimulus bills. Businesses also received cash injections (the biggest first to no one’s surprise), ultimately to the tune of over 2 trillion dollars.

Where did all of this currency come from?

It’s not like it was sitting around in the Treasury (the Treasury typically only has several days of operating cash on hand, sometimes less).

This currency was created by the process detailed previously in this post – only now at scales that dwarf anything we have ever seen in all of monetary history.

This is a short term, macro-view of the steepest part of the hockey stick – and we are solidly on that rocket trajectory and we can’t slow down.

Knowing this, how can we prepare for the eventual settling-up that will inevitably occur from these unsustainable financial practices? Perhaps a time when a wheelbarrow full of cash can barely buy a loaf of bread? It can and does happen.

During the hyper inflation that pre-empted the complete collapse of the mark in the Weimar Republic following World War I, when the value of their currency jumped from 170 marks per ounce of gold to 87 trillion marks per ounce in less than 5 years . Bye bye, savings…

(Table from SodaHead)

{kind=link}

More recently (and ongoing as of this post’s publish date) Venezuela is experiencing a hyper inflation – expected to reach nearly 1,000,000 % this year. The U.S. dollar also shares some blame for this given that the Fed exports its inflation to the rest of the world in exchange for actual finished goods – this is known as the “trade deficit” – but we’ll save that for another time!

How To Protect And Grow Wealth During Financial Crisis

The currently dominant financial paradigm is breaking down underneath its own weight. Debt never was and certainly this time isn’t a sustainable way to give a currency value.

If we are to move into a regenerative economy, one where stewardship of the ecosystems that provide everything for us to live healthy and fulfilling lives is prioritized along with meeting the needs of people so that they may live healthy and fulfilled, we must have a healthy monetary system that incentivizes human action towards those ends.

Healthy money is sound money, not debt-backed fiat currency.

We need to revisit old monetary systems that actually incentivized care of the earth and care for its people (there were actually some good ones!). If we are to have a global monetary system, which in all likelihood we will, it will need to be one that allows an abundance of different systems of account to be tried, tested, fail and ultimately take root where they are best suited.

Just as in an intact forest ecology within which all member species are meeting each other’s needs, competing, cooperating, and processing each other’s wastes, the interconnections between different currencies, money and locally adapted financial paradigms will enable a resilient ecology of human life energy that can be put to work in service of this beautiful place we all call home instead of set to work enslaving it.

While not a monetary system in and of itself, we feel that the 8 Forms Of Capital, a concept originally developed by Ethan Roland of Appleseed Permaculture, provides a principled structure from which truly regenerative monetary systems can be created, evaluated and adjusted as they are refined. In order to create resilient wealth, we must first adopt a new paradigm of what wealth is and why it is worth our life energy to build it.

Read Part 2 of our series on Regenerative Economics – Creating Resilient Wealth With The 8 Forms Of Capital.

Post Categories